A U.S. speeding ticket can feel like a travel problem. For a Canadian driver, it can also become an insurance problem later.

The safer move is not to hide it and hope. If it becomes a conviction, shows up on your record, or comes up in a renewal or application question, a wrong answer can create a bigger problem than the ticket itself.

Most readers are really asking four things at once: what happened, where it can show up, why it matters, and how to handle it without making things worse.

The short answer

A U.S. speeding ticket does not always mean you must call your insurer the same day. But if your insurer, broker, or application asks about convictions, suspensions, cancellations, or driving history, the answer needs to be accurate.

The real risk is not the road trip itself. The real risk is giving an inaccurate answer later when the file is being priced, renewed, or reviewed.

Ontario’s standard auto application asks about convictions in the last three years, licence suspensions or cancellations in the last six years, and past material misrepresentation.

What happens after a U.S. speeding ticket?

First, separate the steps. A ticket is what you receive, while a conviction is what usually matters more for records and insurance.

Misrepresentation means giving incorrect or incomplete information that matters to underwriting or coverage. In plain English, it means the insurer priced or accepted the risk using the wrong facts.

That is why the better question is not “Do I tell Canada?” It is “Did this turn into something I need to disclose when I am asked?”

Where can it show up?

It can show up in more than one place. That is why this topic matters at renewal time.

- your renewal questions

- a new insurance application

- your driving record

- your insurer’s underwriting review

- your premium at renewal

Before accepting a higher renewal, compare insurance quotes in Canada with privacy so you can look at broker bids without giving away your contact details too early.

Why hiding it can cost more than the ticket

A speeding ticket is one problem. A bad disclosure answer can become two problems at once.

If an insurer later decides the information given was incorrect or incomplete, the fallout can include a higher premium, cancellation, or a messy dispute when you need the policy most. That is why guessing is the expensive mistake.

If a U.S. ticket changed your file, the next step is not panic. It is accurate disclosure first, then cleaner comparison shopping on your own terms.

| Situation | What it means | What to do |

|---|---|---|

| You got a ticket in the U.S. but have not dealt with it yet | The final outcome may still change | Confirm the status before answering insurance questions |

| You paid it and it became a conviction | A conviction is more likely to affect record-based underwriting | Keep proof and disclose accurately when asked |

| Renewal asks about convictions | The wording matters more than your assumptions | Answer based on the record, not on where the stop happened |

| You say “no” because it happened outside Canada | That can become a disclosure problem | Correct the answer before the policy is issued or renewed |

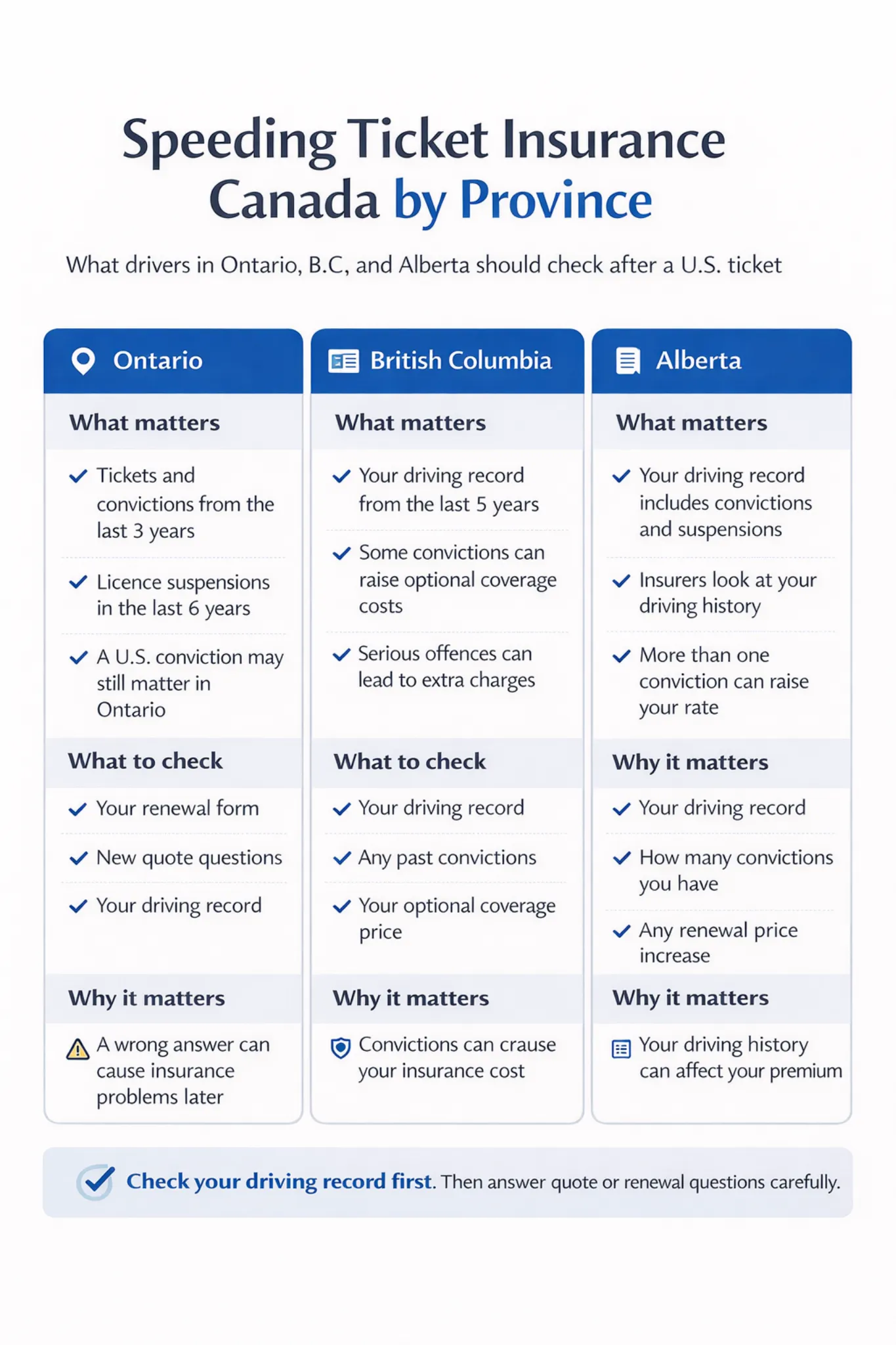

Ontario: where the warning is strongest

Ontario gives this topic the clearest insurance angle. The application wording is direct, and the consequences of a bad answer can outlast the ticket.

Ontario demerit point rules also say those rules can apply if an Ontario resident is convicted or forfeits bail in another province, territory, or a U.S. state. That is enough to warn drivers not to assume a U.S. conviction stays invisible at home.

What Ontario drivers should do

- check whether the U.S. matter became a conviction

- read every conviction question literally

- pull a driver record if renewal is close

- do not assume “outside Canada” means “outside the question”

Ontario drivers may also want to double-check profile details before shopping. Ontario driver’s licence decoder is a free Ontario-only Beat My Insurance tool that reads the last six digits of a licence number to estimate date of birth as a quick reference.

British Columbia and Alberta: what to check

Readers in B.C. and Alberta should take the same practical approach. Treat a U.S. conviction as something worth checking on your record before renewal or quote shopping.

British Columbia

Look at whether the conviction affects your driving record or optional pricing. If renewal is close, pull your record first and make sure your answers line up with it.

Alberta

Think record first, premium second. Before shopping, review your record and ask how any conviction affected rating, tier, or eligibility.

A 3:00 AM scenario

It is 3:00 AM in a hotel parking lot in Buffalo. You pay the speeding ticket online because it feels easier than dealing with court from Canada.

Three months later, your Ontario renewal comes in much higher. You rush through a quote form, answer “no” to a conviction question because the stop happened in the U.S., and turn a manageable ticket into a possible disclosure problem.

What to gather before renewal or a new quote

Have the facts ready before you shop. Better inputs usually lead to fewer mistakes and better conversations.

- driver’s licence information

- current pink slip and policy number

- renewal date

- ticket details

- proof of payment or court outcome

- driving record if needed

- current coverage summary

- questions about how the conviction affects pricing

If you want a faster buying path after you organize your documents, get your insurance quote online fast and keep the process more structured.

| Province | What matters most | Best next step |

|---|---|---|

| Ontario | Application questions about convictions, suspensions, cancellations, and misrepresentation | Read the wording carefully and answer from the record |

| British Columbia | Driving record review and any premium impact tied to convictions | Pull your record before shopping and check how the conviction affects pricing |

| Alberta | Convictions, record details, and risk-based pricing | Review your record and ask how the conviction affected your rate |

What to say to your broker or insurer

You do not need a long script. You need a clear one.

“I got a speeding ticket in the U.S. during a road trip. I want to answer your conviction questions correctly. Here is what happened, here is the outcome, and here is the date.”

That approach shows you are trying to disclose accurately before a wrong answer gets locked into the file. It also makes the next shopping step easier.

If you are deciding how to shop after a ticket, car insurance broker vs direct can help you choose the route that fits a no-longer-perfect driving file.

Why this points naturally to Beat My Insurance

A U.S. speeding ticket does not mean you are out of options. It means the comparison process matters more.

Beat My Insurance is a privacy-first reverse auction marketplace. Buyers share needs first, brokers bid competitively, and buyer contact details are revealed only after a bid is accepted.

That is useful when a ticket changes your renewal and you want real options without repeating your details everywhere. For more context before you decide, browse these auto insurance articles.

Post your needs privately and compare on your terms

If a U.S. speeding ticket changed your renewal, do the disclosure step properly first. Then use a quieter comparison process where brokers compete and your contact details stay private until you accept a bid.

Post Your Auto Insurance NeedsFAQs

Does a U.S. speeding ticket affect insurance in Canada?

It can. What matters most is whether it became a conviction, appears on your record, or falls within the questions asked at renewal or application time.

Do I need to tell my insurance company about a U.S. speeding ticket?

The safest answer is to disclose accurately whenever your insurer or application asks about convictions, suspensions, cancellations, or other underwriting facts. Do not assume “U.S.” means “does not count.”

Can an insurer cancel me for not disclosing it properly?

Incorrect or incomplete information can create serious policy problems. That is why an accurate answer matters more than trying to outguess the system.

Where should I check before renewal?

Check the outcome of the ticket, your driving record if needed, and the wording on the renewal or new application. Those are the three places where mistakes usually start.

Can Ontario drivers use the licence number to estimate date of birth?

Yes, as a quick helper. The Beat My Insurance Ontario-only decoder can estimate date of birth from the last six digits, but it is still smart to verify details against official documents.

How does Beat My Insurance help after a premium jump?

Beat My Insurance gives buyers a privacy-first way to compare broker bids. You share needs first, brokers compete, and contact details stay private until you decide to move forward.

Leave a Reply