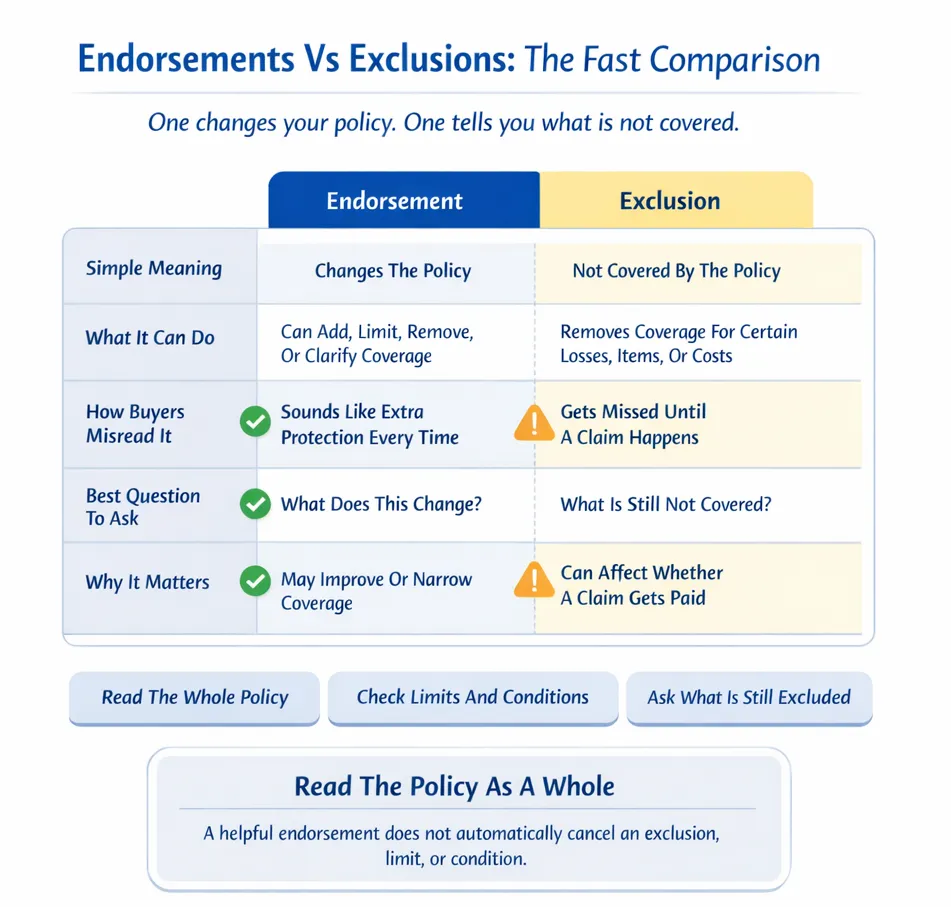

Understanding endorsements vs exclusions in home insurance Canada can help homeowners avoid expensive surprises when they buy, renew, or make a claim. In simple terms, an endorsement changes the policy, while an exclusion tells you what the policy does not cover.

That sounds straightforward, but real life is rarely that clean. One part of the policy may sound helpful, while another part may still limit what gets paid after water damage, a rebuild, or a major loss.

Endorsement: A change to your policy that may add, remove, limit, or clarify coverage.

Exclusion: A loss, item, or cost your policy does not cover.

Not legal advice.

Why This Matters For Homeowners

Most buyers look at price first. That is normal. But price alone does not tell you what happens after a claim.

Two home insurance Canada quotes can look close on premium and still be very different in real life. One may include better water protection, broader contents coverage, or more help with temporary living costs. Another may look cheaper because it has tighter wording, more exclusions, or smaller limits.

A recent Supreme Court of Canada decision made this point very clear. The case reminded homeowners that one helpful sounding policy add-on does not automatically cancel a different part of the policy that limits coverage.

It is 3:00 AM and heavy rain has been falling for hours. By morning, there is water in the basement, damaged flooring, and a long list of questions.

You remember seeing an endorsement on your policy and assume that means the loss will be fully covered. Then the harder question shows up: does that endorsement really apply to this kind of loss, or is there an exclusion, condition, or limit that still changes the outcome?

What Is An Endorsement?

An endorsement is a change to the original policy. It can broaden coverage, narrow coverage, or explain how the insurer will treat a certain risk or item.

This is why an endorsement should never be read as automatic good news. Sometimes it does add useful protection. Sometimes it simply changes the wording in a way that buyers do not fully notice at first.

What Is An Exclusion?

An exclusion is the part of the policy that says what is not covered. It may apply to a type of damage, a category of property, or a specific cost linked to a claim.

This is one of the most important parts of the policy because it answers the question buyers often leave until too late: when will the insurer not pay?

Endorsements Vs Exclusions in Home Insurance Canada

| Policy Term | Simple Meaning | Why It Matters |

|---|---|---|

| Endorsement | A Change To The Policy | It May Add, Limit, Remove, Or Clarify Coverage |

| Exclusion | Something The Policy Does Not Cover | It Tells You What Losses Or Costs Stay Outside The Policy |

| Limit | The Most The Policy Will Pay | You May Be Covered, But Only Up To A Set Amount |

| Deductible | The Amount You Pay First | A Claim Can Still Cost You Money Out Of Pocket |

| Condition | A Rule You Must Follow | Missing A Step Can Affect How A Claim Is Handled |

What The Supreme Court Case Means

The case involved homeowners who believed a rebuilding endorsement should cover extra rebuilding costs after a flood. The Court decided that the endorsement did not override another part of the policy that excluded certain extra costs tied to rebuilding rules.

For regular homeowners, the lesson is simple. A strong sounding endorsement may still sit beside an exclusion, a condition, or a payment limit that matters a lot after a claim.

That does not mean endorsements are pointless. It means the policy has to be read as a whole, not as a collection of isolated phrases.

Where Buyers Usually Get Surprised

Most coverage surprises happen in a short list of areas. These are the parts worth slowing down for before you buy or renew:

- Water Damage

- Sewer Backup

- Overland Flood

- Additional Living Expenses

- Special Limits On Valuables

- Rebuilding Costs

- Changes Since Last Renewal

| Situation | What Buyers Often Think | What They Should Ask |

|---|---|---|

| Basement Water | All Water Damage Is Covered | Is This Covered As Sewer Backup, Overland Flood, Or Something Else? |

| Major Rebuild | Guaranteed Rebuilding Covers Everything | Are Any Rebuilding Costs Still Excluded Or Limited? |

| Living Elsewhere After A Loss | Hotel Costs Are Always Covered | How Much Additional Living Expense Coverage Do I Have? |

| Jewelry Or High Value Items | My Contents Limit Covers Everything | Are There Special Limits For Certain Items? |

| Renewal Time | If The Price Is Similar, The Coverage Is Similar | What Changed In The Wording Since Last Year? |

How To Read A Home Insurance Policy

You do not need to read the policy like a lawyer. You just need a simple order that helps you focus on the parts most likely to affect a claim.

What To Ask Before Buying Or Renewing

Clear questions make the whole process easier. Ask these before you accept any offer:

- What Endorsements Are Included?

- What Exclusions Still Apply?

- Is Sewer Backup Included Or Optional?

- Is Overland Flood Included Or Optional?

- How Much Additional Living Expense Coverage Do I Have?

- Are There Rebuilding Costs That May Still Fall Outside The Policy?

- Are There Special Limits On Jewelry, Tools, Bikes, Or Electronics?

- What Changed Since Last Year?

Why We Built Beat My Insurance This Way

Comparing coverage gets harder when buyers are pushed into calls too early. That is why we built compare insurance quotes in Canada with privacy around a privacy-first reverse auction marketplace where buyers post their needs first, brokers bid competitively, and contact details are only revealed after a bid is accepted.

We believe buyers need room to compare endorsements, exclusions, deductibles, and optional coverages before their phone starts ringing. When the process feels calmer, people usually ask better questions and make better decisions.

If you want the short version of how our buyer flow works, get your insurance quote online explains the process in plain language.

What This Looks Like In Ontario, B.C., And Alberta

Ontario

Ontario is the clearest province example for this topic because the court case came from an Ontario flood loss. If your property is near water or subject to extra rebuilding rules, ask what rebuilding costs are still excluded, limited, or conditional.

British Columbia

In B.C., it is smart to pay extra attention to wildfire risk, temporary living costs, and the exact wording around major losses. The right question is not only “Do I have coverage?” but also “What kind of coverage do I have, and where are the limits?”

Alberta

In Alberta, review local flood and weather risks closely. Make sure you know what is standard, what is optional, and what needs to be added separately before a loss happens.

Simple Checklist Before You Say Yes

- Pull Last Year’s Policy

- Read The Declarations Page

- Highlight Every Endorsement

- Read The Exclusions Carefully

- Check Water Coverage Separately

- Ask About Rebuilding Cost Limits

- Confirm Additional Living Expense Coverage

- Review Deductibles

- Check Special Limits On Valuables

- Compare More Than One Quote On Coverage, Not Just Price

If you want more plain English reading before you compare, our insurance articles cover common buyer questions without the usual noise.

Final Thoughts

The biggest mistake buyers make is assuming a helpful sounding endorsement means the whole issue is covered. That is not always true.

The safer approach is to compare the policy as a whole. Check what was added, what was excluded, what has a limit, and what still needs to be asked before you say yes.

Post Your Home Insurance Needs Privately

When you are comparing home insurance Canada options, there is no reason to hand over your contact details before you are ready. We let you post your needs first, review broker bids, and move forward only when a bid makes sense for you.

Post Your Needs Privately

Leave a Reply