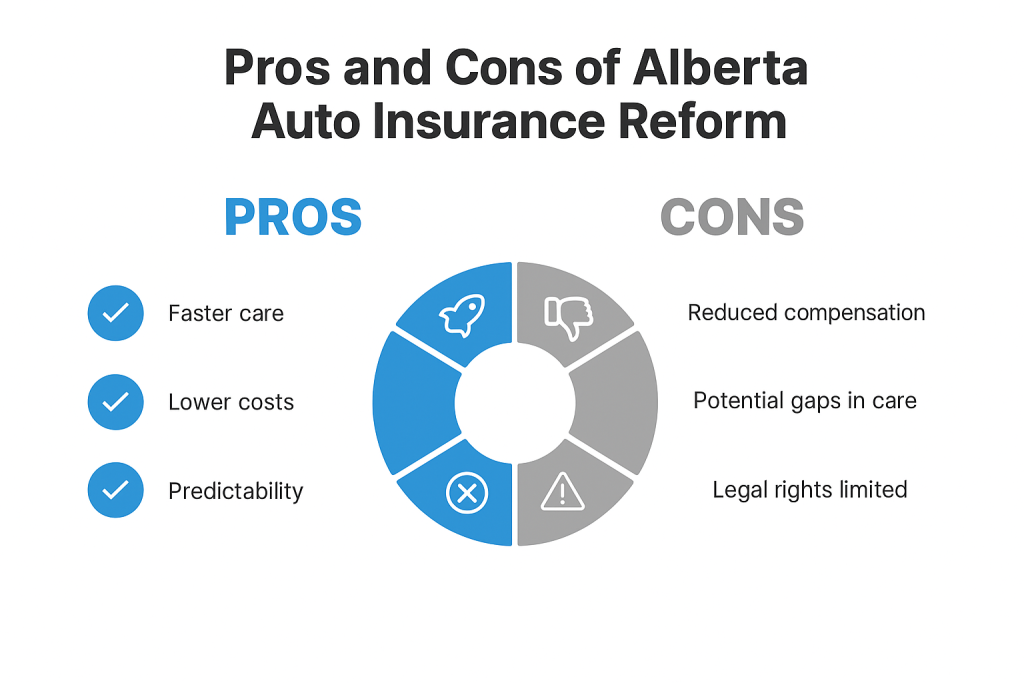

Alberta’s auto insurance system is about to undergo a major overhaul. Starting in 2027, the province plans to switch to a “Care-First” no-fault model. In theory, this means drivers involved in collisions would focus on getting medical care and rehabilitation, rather than fighting over who pays for what. It sounds simple: injured Albertans get help faster, and expensive court battles largely disappear.

But as part of the broader Alberta auto insurance reform, a new debate has ignited around one key question: should injured drivers still have any right to sue the at-fault party?

What Is the Care-First Model?

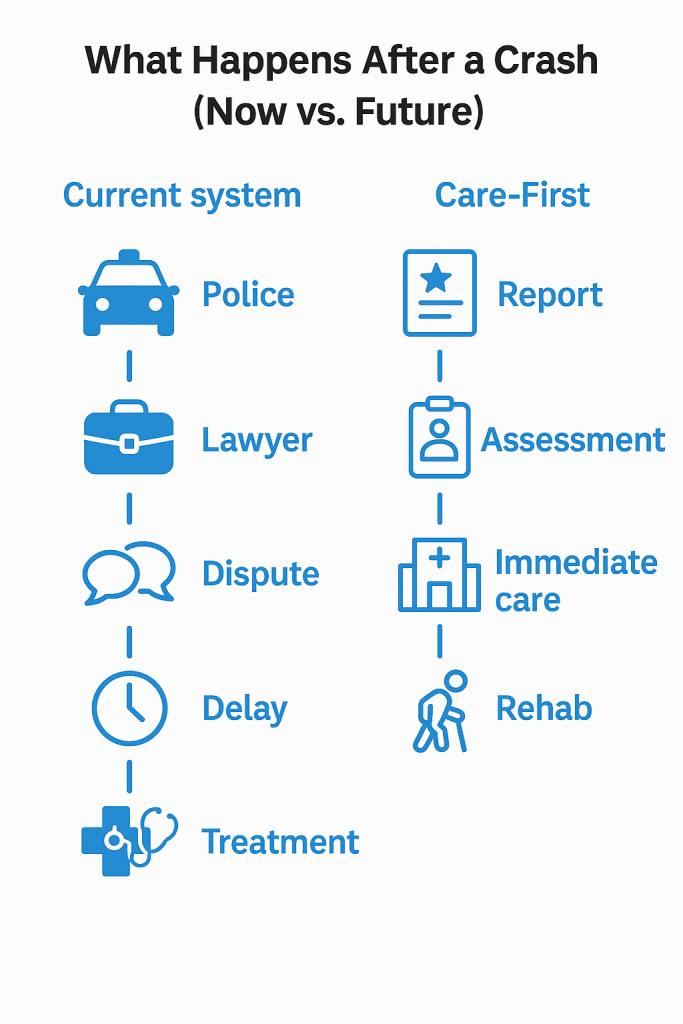

In a traditional (tort-based) insurance system, if you’re hurt in a crash, you typically have to wait for someone to admit fault before your insurer pays for injuries or losses. That often means a lengthy insurance claim or even a lawsuit to settle a claim.

The Care-First model flips this idea: everyone involved goes straight to their own insurer for medical benefits and support, regardless of who caused the accident. The emphasis is on care, doctors, rehab, income support, and so on, without endless legal wrangling.

This isn’t a brand-new idea in Canada. Quebec has had a pure no-fault system for decades and boasts the lowest auto premiums in the country. Manitoba’s public plan and other provinces’ systems also lean heavily on care-focused benefits. Alberta’s version promises to learn from these examples, aiming for quicker access to treatment and more predictable coverage.

In practical terms, most claims would no longer require a court case. Instead, people would see a chiropractor, therapist, or doctor soon after an accident, with insurers paying agreed-upon rates for approved treatments. The hope is that by streamlining the process, overall costs drop and drivers save money on their premiums.

Why Reform Now?

For years, Albertans have faced some of the highest car insurance premiums in Canada. The average cost of coverage in Alberta is roughly in the $1,300 range (compared to about $700 in Quebec, for example). People complain that they pay a fortune for insurance that often doesn’t deliver timely help.

Legal fees, long waits for treatment, and inconsistent claim outcomes have made the system frustrating and expensive. On top of that, the pandemic exposed cracks: backlogs at hospitals and insurers left many accident victims waiting even longer for care.

As part of the push for Alberta auto insurance reform, industry and government figures have pointed out that a lot of money in premiums goes to lawyers and courts – nearly 10 cents of every premium dollar, according to recent data. In practical terms, that’s about $100 of every $1,000 paid by drivers going to legal costs. These overheads ultimately drive up what we all pay at the pump.

With inflation and rising costs of living squeezing household budgets, there’s pressure to find savings. The old system’s complexity has also deterred some insurance companies from competing in Alberta, which further keeps rates high.

At public consultations and in the legislature, officials highlighted the upside of a care-first approach: faster treatment, longer-term support (even lifetime care for catastrophic injuries), and the ability to claim everyday out-of-pocket costs like taxis or medical equipment without having to sue.

The government has promised that, once fully rolled out, drivers will see significant savings – figures like $400 per year on average have been touted. In short, there’s a general agreement that the system needed to change.

The Lawsuit Question: A Costly Compromise?

But here’s where things get tricky. Alberta auto insurance reform is not a pure no-fault system. The province is considering allowing a limited right to sue in certain situations. For example, if the at-fault driver has committed a serious criminal offence like drunk driving, or if someone’s medical bills exceed their coverage limits, then a lawsuit might still be possible. This carve-out was meant to give people some legal recourse for the worst cases.

However, critics warn that even a limited right to sue could undermine the whole model’s savings. Recent analyses commissioned by various groups show a potential jump in premiums if lawsuits are on the table. One report suggests adding back court cases could tack on roughly $120–$218 per driver per year (on top of the premiums drivers already pay).

Another popular number floating around is about $136 extra per year on average. Multiplied across over 3 million Alberta drivers, that quickly adds up to hundreds of millions of dollars. Insurers argue that any extra legal exposure would erode the promised savings and make future rates harder to predict.

From the insurance industry’s viewpoint, having lawsuits in the mix means the system isn’t truly no-fault. It injects uncertainty: every claim could potentially turn into a fight in court. That leads to higher administrative costs, more delays, and the same “battle of the experts” that the care-first model is trying to avoid.

In fact, Alberta’s own data indicate that nearly 10% of our premiums currently cover legal expenses – a huge chunk of the pie. If drivers can sue, insurers say, that percentage won’t shrink by much. Drivers could end up paying more to cover legal fees, rather than seeing it as savings.

Of course, opponents of a full no-fault regime have a counterpoint. They say Albertans should be able to sue to hold wrongdoers accountable and to make sure victims are fully compensated. Removing or limiting that right, even just for certain cases, could leave some people feeling short-changed.

Critics worry that in an extreme accident, a victim might receive all their medical needs met but still miss out on damages for pain, suffering, or lifetime loss of earning capacity. This tension boils down to one big question: Is it better to lock in streamlined care for everyone, or to preserve legal avenues at the risk of higher costs and slower payouts?

Why Drivers Should Care

While the debate might sound abstract, it affects real dollar amounts and real lives. Imagine you’re a driver looking at your insurance bill. An extra $120–$136 a year might not seem earth-shattering for one policyholder. But that’s the equivalent of a bit more than $10 a month. In a big city, it could pay for a couple of tanks of gas or a nice dinner out. For a family with two cars, it doubles. Across the province, those small bumps translate into a lot of money siphoned away from local economies.

Besides the direct cost, there are other consequences to consider. Under the promised care-first system, the goal is that most people will receive consistent, predictable benefits for injuries. You won’t have two people with the same injury getting wildly different payouts just because one decided to sue.

Allowing lawsuits back in means that consistency could fade away. Some injured drivers might still choose to litigate, leading to case-by-case court outcomes. That can drag claims out for years. For an average person who just wants help and closure, this can be stressful and unfair.

On the other hand, supporters of limited lawsuits argue it’s a kind of safety valve. If you truly have a special case – say a loved one lost someone in an accident, or a person is permanently disabled due to gross negligence – the law should let you seek more.

But the counter-argument is that these situations are rare and the no-fault system already plans for extremely serious injuries (often with lifetime care). The worry from many corners is that even giving that small opening to sue will be exploited, turning what was meant to be an exception into a costly norm.

For many Albertans, especially younger families, seniors on fixed incomes, or those still paying off big expenses, the promise of faster and more certain care is appealing. You wouldn’t have to juggle lawyers just to see your doctor. Accident victims could focus on recovery instead of legal strategy.

That can have huge implications for quality of life. Quick treatment means better recovery chances. Knowing exactly what you’re entitled to can reduce stress. These benefits are harder to measure than a dollar amount, but they matter a lot.

Points Drivers Should Know:

- Premium Impact: Studies suggest even limited lawsuit rights could add over $100 extra per year to each driver’s bill.

- Predictability: A strict no-fault model brings similar outcomes for similar injuries. Lawsuits mean unpredictable verdicts.

- Speed of Care: Pure no-fault aims to get you treatment fast. Court cases could slow things down again.

- Scope of Lawsuits: Currently proposed rules would only allow suing for very serious criminal cases or gaps in coverage, not for every fender-bender.

The Bigger Picture: Care vs. Compensation

At the Alberta auto insurance reform, this debate touches on a larger balance of values. Do we prioritize health and efficiency, or do we insist on personal justice and accountability? Different people will answer differently.

- Faster Care, Lower Stress: In Quebec’s system (often held up as an example), accident victims typically get access to medical and rehab benefits very quickly. There are no lawyers involved in most cases, which means people report less stress and delays. The trade-off is that they can’t sue for pain and suffering or loss beyond what the system covers. Overall, Quebecers enjoy the lowest average premiums in Canada, partly because legal costs are minimal.

- Legal Rights, Bigger Payouts (if you win): In a pure fault system, if you win a lawsuit, you might recover significant additional damages. This can feel fair if someone’s negligence caused your life to change. However, research has shown that the legal process is often slow and unpredictable. Lawyers take a cut, cases sometimes settle for less than expected, and the insurance costs for everyone tend to be higher to pay for those risks.

Alberta auto insurance reform is trying to thread the needle between these models. It promises many of the no-fault perks like care until recovery and streamlined claims, while preserving a bit of the fault system’s muscle. But every side agrees there’s a trade-off. If litigation stays in the picture, even a little, it looks a lot like the old system with a few tweaks. If litigation goes on, some people worry only about whether the government’s care promises will be enough.

One thing almost everyone mentions: nothing is set in stone yet. The government plans extensive consultations, and the final plan is still being written. This gives drivers a chance to learn the details and speak up. Insurers and legal groups are already lobbying and releasing studies, hoping to sway the outcome.

What’s at Stake for the Future?

The new Alberta auto insurance reform will likely govern how insurance claims are handled for decades. If the province lets lawsuits linger in the system, we might find ourselves paying something closer to today’s premiums a few years from now. If it cuts off litigation almost entirely, it will need to build a bulletproof benefits program that truly covers what injured people need.

It’s also a matter of trust. If drivers feel the Alberta auto insurance reform is being shaped behind closed doors or driven by lobbyists, public faith could erode.

Policymakers have said they want this system to reflect what Albertans want. So far, different surveys give mixed messages: some polls show most people still like the idea of suing at-fault drivers, while others emphasize wanting lower costs and faster care.

The key will be public education. Drivers should pay attention to how the plan is written, what exceptions are allowed, and whether the promised cuts in rates actually materialize after 2027.

Educating all stakeholders is crucial. Drivers need to understand exactly how claims will work in real terms. Insurers should explain how they will manage these care packages and maintain competition. Doctors, therapists, and other care providers need to know how their payments and roles might change.

And lawyers, who may have a smaller role under a no-fault model, will also have to adjust. Bringing everyone to the table for open discussion will help smooth the transition.

Finally, there’s the question of precedent. Alberta’s decisions here could influence other provinces debating their own insurance models. If Alberta successfully bends the curve downward and backs it up with solid care programs, other provinces might feel pressure to follow suit. If it stumbles, it will reinforce the status quo elsewhere. So, what happens in the next year or two doesn’t just affect us here – it could tip the scales nationally.

Take Control: Compare Auto Insurance with BeatMyInsurance.com

Due to Alberta auto insurance reform, now’s a smart time to reevaluate your own coverage. If you’re curious about potential savings or just want to see what’s out there, BeatMyInsurance.com makes it easy.

You simply upload your insurance needs, like your current policy or what you’re looking for, and stay completely anonymous while licensed providers review and send you quotes. You only reveal your identity if you accept a quote. That means no spam calls, no pressure, and no commitment until you’re ready.

It’s a stress-free way to compare offers side by side and potentially beat your current rate, especially as Alberta’s market prepares for changes.

- Stay private

- Compare real offers

- Make a smart choice on your own terms

Visit BeatMyInsurance.com to see what’s possible, before the Alberta auto insurance reform takes effect.

Conclusion

The Alberta auto insurance reform is meant to be a win-win: faster, better care for accident victims and lower costs for drivers. However, even a small right to sue remains a hot-button issue. Insurance analysts warn that keeping litigation alive could chip away at the projected savings, turning a big premium cut into a modest one, or even none at all. Supporters of the lawsuit carve-out argue it’s a needed safety net for the worst cases. Opponents say it’s a loophole that could sink the whole ship.

For everyday Albertans, the stakes are tangible. This debate will help decide whether your next car insurance bill is noticeably cheaper and whether getting into a crash means immediate treatment or a legal drama. If the government and industry get it right, drivers could see real relief: more affordable rates and less paperwork when they need help. If they get it wrong, we might end up paying almost as much as we do now, without gaining much besides bureaucratic complexity.

The outcome isn’t just a matter of policy wonks hashing out details; it will affect thousands of families, businesses, and communities. As the Alberta auto insurance reform takes shape, Albertans should stay informed, ask questions, and voice their views. After all, once this new system is in place, it will shape our roads and wallets for a generation to come.

Leave a Reply